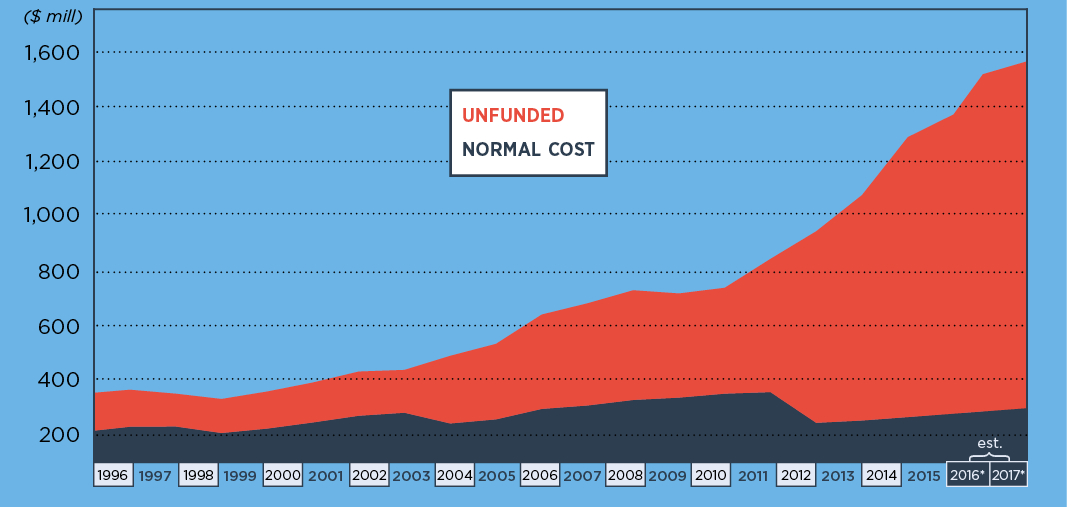

Unfunded Liability in the State Employees Retirement System (SERS)

What are Liabilities?

Liabilities are legal debts and obligations that the state has incurred. The state’s two largest categories of liabilities include outstanding debt (bonds, long-term notes, etc.) and post-employment benefits for employees (pensions, retiree health care, etc.). On this page you will find direct links to reports detailing specific state liabilities including pension actuarial reports, other post-employment benefit actuarial reports and the state’s Comprehensive Annual Financial Report which provides a full detail of the state’s financial position.

Retirement Systems Actuarial Reports

Teachers’ Retirement System Actuarial Reports

Other Post-Employment Benefits Actuarial Reports

Comprehensive Annual Financial Reports

BOND ALLOCATION

View the state’s Bond Allocation Database, maintained by the Office of the State Comptroller.

The Bond Allocation Database contains information about projects that have been approved by the State Bond Commission at its monthly meetings between January 1995 and the present.

More helpful links:

- Members of the Bond Commission

- Agendas for recent Bond Commission meetings

- An explanation of how the bond allocation process works

- An explanation of the limitations of the bond database

WHAT ARE BONDS?

The state raises money for certain projects by issuing bonds. In the simplest terms, bonds are a form of debt. They are sold to investors and obligate the state to pay a specified rate of interest during the life of the bond and to repay the principal or face value of the bond on a set date in the future.

In state finance, there are two primary types of bonds, general obligation (GO) bonds and revenue bonds. For general obligation bonds, the debt is secured by the state’s power to tax. In other words, the state pledges its full faith and credit for payment of principal and interest. For revenue bonds, the state identifies and pledges a specific revenue source for payment of principal and interest.

WHAT IS A BOND ALLOCATION?

After enabling legislation – known as a bond authorization – is enacted, agencies still need approval from the State Bond Commission in order to commit funds for specific projects. This approval is known as a “bond allocation” and these allocations are what the searchable bond allocation database above tracks.

WHY IS THIS INFORMATION IMPORTANT?

In short, because it’s your money! Most of the attention state government finance receives – whether by analysts, the media or the public – is focused on the state’s General Fund which accounts for about 85% of the state’s total operating budget.. General Fund operations are financed through various types of tax receipts, federal grants, and other sources.

At the same time, a significant amount of state spending is financed through borrowing. Even though billions of dollars are involved, until now, it has been quite difficult for the general public to track how those dollars are spent.