| The Comptroller's Report |

Nancy Wyman - State Comptroller

|

Connecticut's Financial Position:

From Deficit to Surplus and Back Again

Connecticut state government uses two different accounting methods to assess

and report its fiscal condition. One method is referred to as Generally Accepted

Accounting Principles (GAAP); the other is known as modified cash accounting.

GAAP, as the name implies, is the recognized standard for accurate financial

reporting. Corporate financial reports that many readers are familiar with are

based on GAAP.

Connecticut state government has not yet adopted GAAP for budget or financial

control purposes. Instead the state uses the modified cash system to prepare the

budget and to control and report spending and receipts through the year.

The state's fiscal condition under modified cash accounting is dependent on

relatively unsystematic timing of payments and posting of receipts. GAAP

utilizes more rigid standards on when to post expenditures and record revenue.

Therefore, GAAP provides a more consistent and reliable method for reporting and

analyzing state financial data. Accordingly, the fiscal data that follows is

presented on a GAAP basis.

Because the state budget is presently based on modified cash accounting, the

media tends to report the state's position on this cash basis. Therefore, the

GAAP numbers that follow may surprise some readers.

Fiscal Year 2001 General Fund Performance -

Operating Results for One State

Fund in a Single Fiscal Year (July 1, 2000 - June 30, 2001)

- The General Fund is the state's largest single operating fund. Most state

programs and revenues are accounted for within the General Fund. Almost 90

percent of all state operating expenses are within this single fund.

- In Fiscal Year 2001, the state recorded a General Fund surplus of $13

million with revenues totaling $13.066 billion and expenditures of $13.053

billion. The surplus is equal to less than one-tenth of 1 percent of

expenditures.

- Since the introduction of the income tax in Fiscal Year 1992, the state's

cumulative General Fund surpluses total to $769 million.

- At the end of Fiscal Year 2001 the sum of $30.7 million was placed in the

state's Rainy Day Fund bringing the fund balance to $594.7 million. This

fund is targeted to hold reserves equal to 5 percent of budgeted General Fund

spending for the year. In 1987, the Rainy Day Fund had a balance of $319.6

million. Three consecutive fiscal years of withdrawals between 1988 and 1990

wiped the fund out.

- With no available Rainy Day Fund reserves by 1991 and a deepening

recession, the state was forced to borrow close to $1 billion in order to

close a budget hole. An expanded revenue base with the introduction of the

income tax in Fiscal Year 1992 and a gradually improving economy allowed the

state to pay off this debt over the six years that followed. Deposits to the

Rainy Day Fund have been made annually since 1995.

- Today, the state's revenue base, dollar reserves, and economic potential

are in a far stronger position than in the early 1990s.

General Fund Revenues:

- In Fiscal Year 2001, total General Fund revenue grew 5.9 percent or $730

million over the prior year. The income tax and the sales tax, which totaled

$7.3 billion in Fiscal Year 2001 and accounted for well over half of all

revenue, increased by 11.4 percent and 0.4 percent respectively from the prior

year.

- The current economic recession began in March 2001, which impacted the

final quarter of Fiscal Year 2001. The downturn reduced sales tax receipts

toward the end of the fiscal year. Income tax receipts were not impacted as

quickly or as severely by the recent downturn.

- Tax reductions over the past six years have reduced revenue by over $1

billion. The tax reductions have been broad based including direct rebates,

lower income tax rates at various income levels, a property tax credit,

substantial reductions in corporation taxes, additional sales tax exemptions,

and hospital tax relief.

- Not all General Fund revenue comes from taxes. Taxes accounted for 66

percent of the total. Federal payments to the state contributed another 24

percent. The remaining 10 percent of General Fund revenues consisted of casino

and lottery receipts, interest earnings, licenses, fees, investment earnings,

fines and forfeitures, charges and other miscellaneous items.

- Of the major General Fund revenue sources, the income tax has experienced

the highest rate of increase with five-year average annual compounded growth

of 10.1 percent. Strong employment gains coupled with booming financial

markets over the five-year period explain the increase. Of the smaller revenue

sources, casino payments have seen the strongest growth advancing at a

five-year average annual compounded rate of 17.4 percent.

General Fund Expenditures:

- In Fiscal Year 2001, General Fund spending increased by $640 million or 5.2

percent over last fiscal year.

- For the fourth straight year the state's constitutional cap on spending

was lifted under provisions of law. The additional spending required a

declaration of extraordinary circumstances by the Governor. Over the past four

fiscal years the cap has been lifted in order to permit over $1.5 billion in

additional state spending.

- Increases above the average growth rate of 5.2 percent for Fiscal Year 2001

occurred in education, health and hospitals, judicial programs and general

administration; below average growth occurred in human services and regulation

and conservation programs. Looking at growth rates over the five-year period

prior to Fiscal Year 2001, the only areas to experience annual growth rates of

less than 5 percent were human services and education.

- Over the past five fiscal years, General Fund spending has increased at a

compounded annual rate of 5.43 percent.

- Two-thirds of all General Fund spending is directed to education, health,

and human services programs. These program areas include education grants to

towns, higher education institutions, mental health and mental retardation

services, nursing homes, income support and health insurance for disabled and

low-income individuals.

Beyond The General Fund - Total Governmental Operations

The state undertakes various activities that do not appear in the General

Fund. These activities include transportation and housing programs, grants to

municipalities for school construction and other needs, loan programs and other

services. When these activities are combined with those of the General Fund, a

more complete picture of state governmental operations emerges.

- Combined governmental operating results for Fiscal Year 2001 show a deficit

of $505 million. On a positive note, this is an improvement of $110 million

from the prior fiscal year.

- Operating deficits of $417 million were incurred in the grants and loan

programs and housing programs. The shortfalls must be covered through debt

financing. Issuing bonds to cover annual grants, loans and housing programs

that have become a part of ongoing state operations is a dubious financial

practice. As can be seen from the debt section that follows, controlling state

borrowing is a major challenge facing government.

Cumulative Financial Position of the State -The Balance Sheet

In evaluating the state's fiscal health, there is a tendency to focus

exclusively on a single year of state operations. This approach fails to provide

a long-term view of the state's financial position. The balance sheet provides

this perspective. The balance sheet shows total state assets, liabilities, and

fund balances at the close of each fiscal year.

- At the end of Fiscal Year 2001, the General Fund balance sheet displayed a

cumulative GAAP deficit of $782 million. This represents a $107 million

increase over last year.

- The main reason for the balance sheet deficit is the state's continued

reliance on an unusual system of budgeting. The state's modified cash

accounting system that is used for budgeting purposes allows some revenues to

be counted before they are earned while some expenditures are not counted for

months after the liability arises. When GAAP corrections to the assets and

liabilities are made a deficit results.

- The GAAP deficit is an important number because those who invest in

Connecticut's bonds and notes review it. If the state's GAAP deficit is

perceived to present investment risk, the interest payments on the debt will

rise costing state taxpayers millions of dollars more.

- The way to improve the state's balance sheet position is clear: adopt

GAAP as the legal basis for state budgeting.

Debt Position

- Connecticut continues to lead the nation in state tax supported debt per

capita. Bonded debt per capita has more than doubled over the past decade

growing to $2,994 at the end of Fiscal Year 2001. This is the amount of money

that every man, women and child would have to pay to eliminate the state's

outstanding debt.

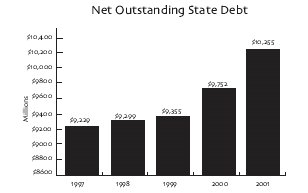

- In Fiscal Year 2001, the state added an additional $503 million to its net

outstanding bonded debt total. Net state bonded debt rose to $10.3 billion by

the end of Fiscal Year 2001.

- In Fiscal Year 2001, the state issued $1.327 billion in new debt. Of this

total $816 million was for infrastructure or other assets benefiting future

generations of taxpayers. The remaining $511 million was used to fund on-going

state operating expenses. Bonding for special projects that provide tangible

benefits to future generations is justifiable; bonding for ongoing programs

that should be considered part of normal government operating expenses is not

sound fiscal policy.

- Large amounts of debt require high annual debt service (principal and

interest) payments. In Fiscal Year 2001, debt service payments totaled $1.34

billion with $790 million paid toward principal and $550 million in interest

payments.

- Debt service is a fixed cost that cannot be quickly adjusted when state

revenue growth slows and budget deficits are projected. In difficult economic

times a high debt load can cripple a state's ability to respond effectively

to the fiscal challenges it faces.

- Bonded debt represents about 60 percent of the state's total long-term

debt obligations. In Fiscal Year 2001, state long-term debt obligations

totaled $17.52 billion.

- The decline in total long-term debt since Fiscal Year 2000 is largely due

to exceptional earnings on assets in the pension funds thus reducing the

difference between the amount ultimately payable to employees and the assets

on hand to meet those payments. This difference is known as the unfunded

pension liability.

Table

of Contents | Index of Comptroller's

Reports | Comptroller's Home

Page