Comptroller Kevin Lembo Archive > News

COMPTROLLER LEMBO PROJECTS $8.7-MILLION SURPLUS WITH CAUTIONComptroller Kevin Lembo today announced that the state is currently on track to end the fiscal year with an $8.7-million surplus, but he warned that this projection is based on consensus revenue estimates that rely on the optimistic view that final income tax payments will perform better than estimated income tax payments have performed so far.

In a letter to Gov. Dannel P. Malloy, Lembo said that his surplus projection is slightly lower than the Office of Policy and Management’s (OPM) due to a variance in estimated claims expenditures in the adjudicated claims account related to settlement payments in the SEBAC vs. Rowland case. While OPM projected claims expenditures to be $9 million, Lembo said there is a chance that it could reach $23.6 million if settlement payments are not delayed.

The outlook has improved this month following Jan. 17 consensus revenue projections – estimates reached in consensus by OPM and the legislature’s nonpartisan Office of Fiscal Analysis (OFA).

“A surplus projection is always good news, though it comes with caution – both for the short and long-term outlook – because it is largely driven by one-time revenue windfalls from legal settlements and possibly optimistic views about final income tax payments,” Lembo said. “I am concerned that the January consensus forecast relies on strong April income tax receipts.

“Estimated income tax payments through January were below last fiscal year’s receipts. Typically, final April payments trend in the same direction as estimated payments – however, because of stock market corrections and subdued bonus payments in the 2015 tax year, a large number of taxpayers may be eligible to utilize safe harbor provisions in the tax code, which allows taxpayers to delay the payment of their full 2016 tax liability until April of 2017, rather than incorporating the payment into their fourth-quarter 2016 estimated payments.

“This would help to explain why estimated payments remain negative despite a strong stock market run-up in the final months of the 2016 tax year. In addition to the uncertainty with respect to final income tax payments in April, the growth in the payroll-driven withholding portion of the income tax has been slowing. Therefore, income tax receipts remain a significant risk factor to the current surplus.”

The consensus revenue projections increased General Fund receipts by $56.7 million, while OPM is also expecting net General Fund spending to fall $8.2 million below last month’s figure.

The most significant revenue shortfalls from the original Fiscal Year 2017 budget are in the income tax (down $81.5 million) and the sales tax (down $79.3 million). The largest tax revenue gain from the initial budget target is in the corporation tax (up $80 million) and the miscellaneous revenue category has grown by $111.5 million due to one-time settlement payments to the state.

Meanwhile, General Fund spending was running 2.1 percent of $161.3 million below the same period last fiscal year.

“A continuation of this spending trend could help offset the higher adjudicated claims estimate from SEBAC vs. Rowland, and mitigate potential future revenue shortfalls,” Lembo said. “Connecticut’s overall budget performance is ultimately dependent upon the performance of the national and state economies.”

Lembo pointed to some of the latest economic indicators from federal and state Departments of Labor and other sources that show:

• In Fiscal Year 2016 the withholding portion of the income tax increased 3.4 percent from the prior fiscal year. Through December of Fiscal Year 2017, these receipts were up 2.4 percent from last year. Adjusting for timing differences between fiscal years in deposit days by month, the withholding tax trend has been running at or below 3 percent.

• Preliminary Connecticut nonfarm job estimates from the business

establishment survey administered by the U.S. Bureau of Labor Statistics (BLS)

show the state lost 1,700 payroll jobs in December 2016 to a level of 1,678,000,

seasonally adjusted. November’s initial job gain figure of 2,100 jobs was

adjusted down to show a gain of 1,900 jobs.

• The establishment survey indicates that the state has lost 2,000 payroll

positions over the past twelve-month period ending in December. It should be

noted that this survey has been subject to major revisions in past years when it

has been benchmarked for the full calendar year. The 2016 revisions will be

released by BLS on March 13, 2017.

• Other data, including withholding receipts and the household census survey,

indicate Connecticut’s job performance has been better than the establishment

survey has indicated. The household survey shows Connecticut adding almost 4,000

jobs in December and up almost 32,000 jobs for the 2016 calendar year.

• Based on the establishment survey, Connecticut has now recovered 70.4 percent

or 83,800 of the 119,100 jobs lost to the Great Recession.

• As the state’s employment recovery has progressed, an increasing number of job

sectors have posted employment gains. However, this month’s data from the

establishment survey has reversed some of the strong sector-wide gains that had

been recorded over the past many months. The actual results will not be known

until benchmarking is completed.

• U.S. employment has been advancing at a rate of 1.5 percent over the

12-month period ending in December; Connecticut’s employment growth pending

final benchmark adjustment was a negative 0.1 percent during that period.

• Connecticut’s unemployment rate was 4.4 percent in December (which comes from

the household survey that has been showing job gains in Connecticut); the

national unemployment rate was 4.7 percent. The declining unemployment rate this

month is another artifact of the inconsistency in Connecticut data between the

establishment employment survey and the household survey. Connecticut’s

unemployment rate has continued to decline from a high of 9.5 percent in October

2010.

• There were 83,500 unemployed job seekers in Connecticut in November. A low of

36,500 unemployed workers was recorded in October of 2000. The number of

unemployed workers hit a recessionary high of 177,200 in December of 2010.

• All of the employment and related data must be considered in light of the

erosion in the state’s total population over recent years. According to U.S.

census date, Connecticut saw a decline in population of 8,278 residents between

July 1, 2015 and July 1, 2016. Connecticut was one of only eight states to

experience a decline in population during this period. Connecticut has now

posted three consecutive years of population decline.

![]()

• Average hourly earnings at $30.59, not seasonally adjusted, were up $0.79, or

2.6 percent, from the December 2016 hourly earnings estimate. The resultant

average private sector weekly pay amounted to $1,030.88, up $29.60, or 3.0

percent higher than a year ago.

• Connecticut ranked 11th nationally in income growth for the 3rd quarter of

2016 based on personal income statistics released by the Bureau of Economic

Analysis on Dec. 20. Among the New England states, only Massachusetts and New

Hampshire outpaced Connecticut’s growth. Connecticut’s annualized personal

income growth based on 3rd quarter results was 4.9 percent. While this is still

off the pace of the last recovery period, it continues a recent pattern of

quarterly improvement.

• Personal income statistics for 4th quarter personal income growth will be

released on March 28.

• According to a Jan. 24 release from CT Realtors, Connecticut single-family

residential home sales increased 2.4 percent in December 2016 from the same

month a year earlier. The median sale price also posted an increase of 3.6

percent to $248,750. This marks the fourth consecutive month of price increases,

and it reverses a persistent trend of monthly declines in home prices over the

past several years. Townhouse and condominium sales increased 12.4 percent in

December and prices increased 14.1 percent to $166,000.

• The National Association of Realtors (NAR) reported that U.S. sales of

existing homes including condominiums had the best sales volume in more than a

decade. This came despite a 2.8 percent decline in December sales. The median

price for existing homes in December was up 4% to $232,200. This was the 58th

consecutive month of price increase.

• A solid national job market and exceptionally low mortgage rates are credited

with the solid national housing performance in 2016. The December slowdown is

attributed to some upward movement in interest rates, rising home prices, and

low inventories. Inventory dropped by almost 11 percent in December, inventories

are at the lowest level since 1999 when the Association began tracking inventory

totals.

Consumers

• Retail spending growth advanced a strong 0.6 percent in December from the

previous month, and 4.1 percent from December of 2015. Sales for 2016 were up

3.3 percent from 2015.

• The strongest December gains were posted in non-store retailers (on-line

shopping) and car dealers. Department stores once again suffered the largest

drop in consumer spending.

• The chart below shows the last three months of retail sales activity, with a

focus on sales excluding and including automobiles.

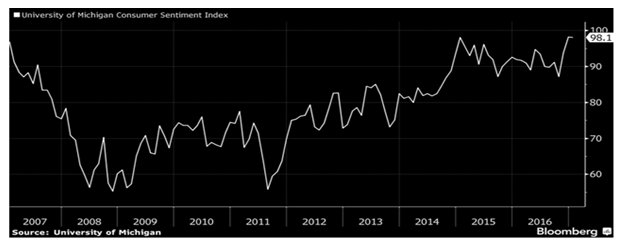

• Consumer confidence in January 2017 is at its highest level at the start of

a new year since 2004.

• The current conditions index, which measures Americans’ perceptions of their

personal finances, increased to 112.5 from 111.9 in the prior month.

• The gauge of expectations six months from now declined to 88.9 from 89.5 in

December that was the highest in almost two years.

• The Federal Reserve Bank reported on Jan. 9 that consumer credit expanded at a

seasonally adjusted annual rate of 7.9 percent, or $24.6 billion, in November.

Revolving credit like credit cards jumped 13.5 percent while non-revolving

credit such as car and student loans rose 5.9 percent.

Business and Economic Growth

• According to the Jan. 27 advance estimate from the Bureau of Economic

Analysis, GDP in the 4th quarter of 2016 grew at a 1.9 percent annual rate. The

growth rate in the 3rd quarter was 3.5 percent.

• The deceleration in real GDP in the fourth quarter reflected a downturn in

exports, an acceleration in imports, a deceleration in personal consumption

expenditures, and a downturn in federal government spending that were partly

offset by an upturn in residential fixed investment, an acceleration in private

inventory investment, an upturn in state and local government spending, and an

acceleration in nonresidential fixed investment.

• Corporate profits also continued rebounding in the 3rd quarter. Profits

rose 5.8 percent on a quarterly basis and were 2.1 percent above the 3rd quarter

of last year.

• Third-quarter earnings gains were led by technology, utilities, basic

materials, financial and consumer-discretionary companies. Real estate, health

care and financials showed the most improvement in revenue.

• Corporate profits have been constrained in recent years by various forces

including weak global growth, a strong dollar, and slumping commodity prices

that contracted the energy and agriculture sectors. But business earnings have

shown signs of stabilization this year as some of those past pressures have

weakened.

• The Commerce Department reported that orders for durable goods—products

designed to last longer than three years, such as machinery or minivans—fell 0.4

percent in December from a month earlier to a seasonally adjusted $227.02

billion.

• The decline was unexpected. Economists surveyed by The Wall Street Journal had

forecast a 2.3 percent increase in overall orders. But orders for defense

capital goods, a highly volatile category, fell 33.4 percent last month, the

largest one-month drop since May 2014.

• Excluding defense, orders rose a healthier 1.7 percent in December from

November. For all of 2016, overall durable-goods orders fell 0.3 percent from

the prior year.

• An important proxy for business investment, orders for nondefense capital

goods excluding aircraft, rose 0.8 percent last month, the third straight

monthly increase. Orders in the category still fell for the year.

• The service-sector, which is the largest sector of the economy, continued to

growth in January. The Markit Flash Services PMI signaled a positive start to

2017. Service providers were more upbeat about the business outlook than at any

time since May 2015. Inflationary pressures eased in December but have generally

been at higher levels over the last year-and-a-half. There was also a strong

increase in new work orders.

Stock Market

• Estimated and final income tax payments account for approximately 40

percent of total state income tax receipts. Both the estimated and final

payments had a negative rate of growth in Fiscal Year 2016.

• The two large estimated income tax payments for Fiscal Year 2017 have been

deposited. Estimated payments through the 3rd week of January, net of accrual

activity, were down 9.2 percent from last year. As can been seen from the graph,

it is typical for final income tax payments to follow the direction of estimated

payments. The bulk of final payments will not be received until April.

• Current consensus revenue estimates rely on positive growth in final income

tax payments in Fiscal Year 2017. Because of the suppressed tax liability in the

2015 tax year due in part to significant stock market corrections, it is assumed

that taxpayers may apply safe harbor provisions to delay the payment of their

full 2016 tax liability until April.

• The graphs below show the year-to-date movement in the DOW and the S&P

respectively at this writing.